Dino Polska - Compounder of note

Our featured, quality company is Dino Polska SA, a Polish grocery retailer, founded in 1999 and started to expand exponentially from 2010. The company has a unique business model providing opportunities to re-invest all its free cash flow in expanding the business. The most appropriate form of capital allocation from an investors perspective.

At December 2023, the group comprises 2,406 stores, opening on average of 247 stores per annum over the preceding 5 calendar years. Their operational execution, exceptional logistics, modern IT systems and track record of successfully opening stores, are some of their key strengths.

Annual growth in sales area in square meters. LTM is the last 12 months to 31 March 2024, this is traditionally the slower period for construction over winter.

The business model is for a standard size store of 400 square meters, staffing of 12 employees per store, and an approximate primary catchment area of 3500 shoppers. It utilises a distribution centre for every 350 stores served by a dedicated meat processing facility, daily fresh meat an important offering to Polish clients. Each store carries a maximum of 5000 SKU’s (stock items) split by revenue as follows: 40% fresh produce, 48% other groceries and 12% other items. All the stores are in less urbanised areas such as small towns, villages and suburban districts. The company owns 95% of all its premises, unique amongst its competitors.

Like for like sales in existing stores grew an average of 16% pa over the last 5 years.

The company listed in 2017 and its founder, Thomas Biernacki still owns 51% of the shares. The company has low levels of debt with all of the free cash flow applied to expansion. A true compounder.

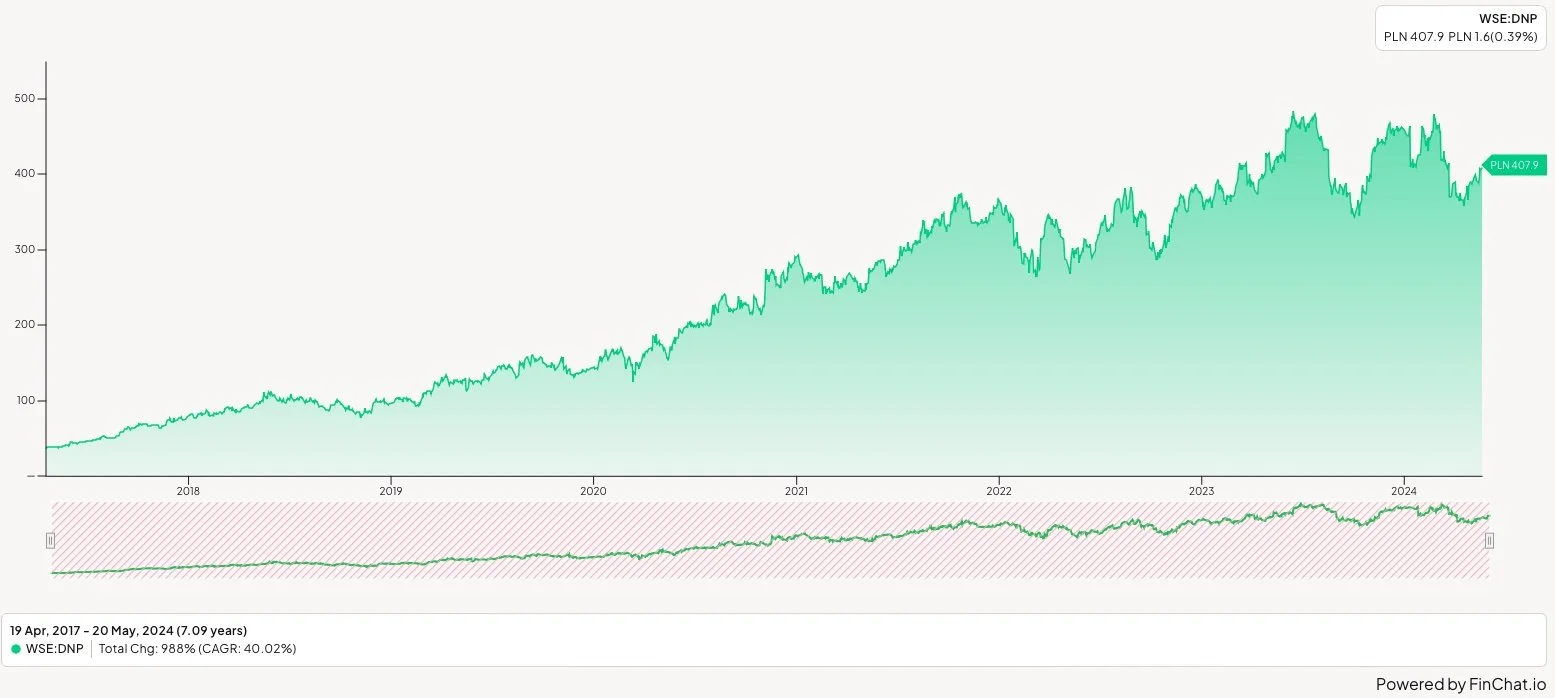

Since listing April 2017, the share-price has grown at a CAGR of 40.02%.

DNP share price since listing

One page analysis on the business:

Valuation thoughts

At the current share price of PLN 407.9, our valuation of Dino Polska, at a discount rate of 10% and terminal growth rate of 3% indicates an implied growth rate in free cash flow of 8.75% over the next 10 years. Working with a margin of safety our outlook is that DNP will grow its net earnings between 18% to 22% over the next 5 to 10 years. Provided this growth in EPS materialises, the current share price is cheap.

The major risk to DNP is whether it can keep up the impressive growth in net earnings over the next few years. With managements track record and their stated intent to continue expanding, and improving its operating margins, we believe DNP to be a quality company at a reasonable price.

Disclaimer: The information provided on this page is for informational purposes only and should not be interpreted as investment advice or as a recommendation to buy or sell any stocks. It merely reflects our views on the companies we have analysed and in certain instances in which we have invested or whose shares we have divested. Please note that the past performance is not indicative of future outcomes and should not be relied upon as such.