MSCI - More than just a name

Our continuous search for quality companies has led us to MSCI Inc. The company’s compounded annual growth rate, (CAGR), amounts to 20% p.a. (excl. dividends), since its listing in 2008. It has long serving, experienced management team, that has produced a return on invested capital of 25% annually over the last 5 years, with a low capital intensity and converts more than 100% of its annual earnings into free cash flow every year. All things we like!

The growth in the number of ETF’s worldwide has been astronomical, in addition to companies that issue the ETF’s, the other great winners in this race are those that benefit from providing the Index details and lending their names to the various ETF’s that track their indices, MSCI Inc being one.

“In 2024, ETF assets in the United States crested the $10 trillion mark, representing a 400% increase over the past decade. Although that increase in total assets includes market appreciation, the growth trajectory is like nothing the financial services industry has seen.

There are now more than 4,000 ETFs trading in the U.S., a total bolstered by a record 650 ETF debuts last year, which beat the previous year’s record for launches by 150 ETFs.”

MSCI Inc., originally known as Morgan Stanley Capital International, was spun off from Morgan Stanley in 2009. Founded in 1969, MSCI Inc. is a leading provider of critical decision support tools and services for the global investment community. The company is renowned for its expertise in research, data, and technology, which helps clients build better investment portfolios. MSCI's offerings include indexes, portfolio risk and performance analytics, and ESG (Environmental, Social, and Governance) research, and private asset research.

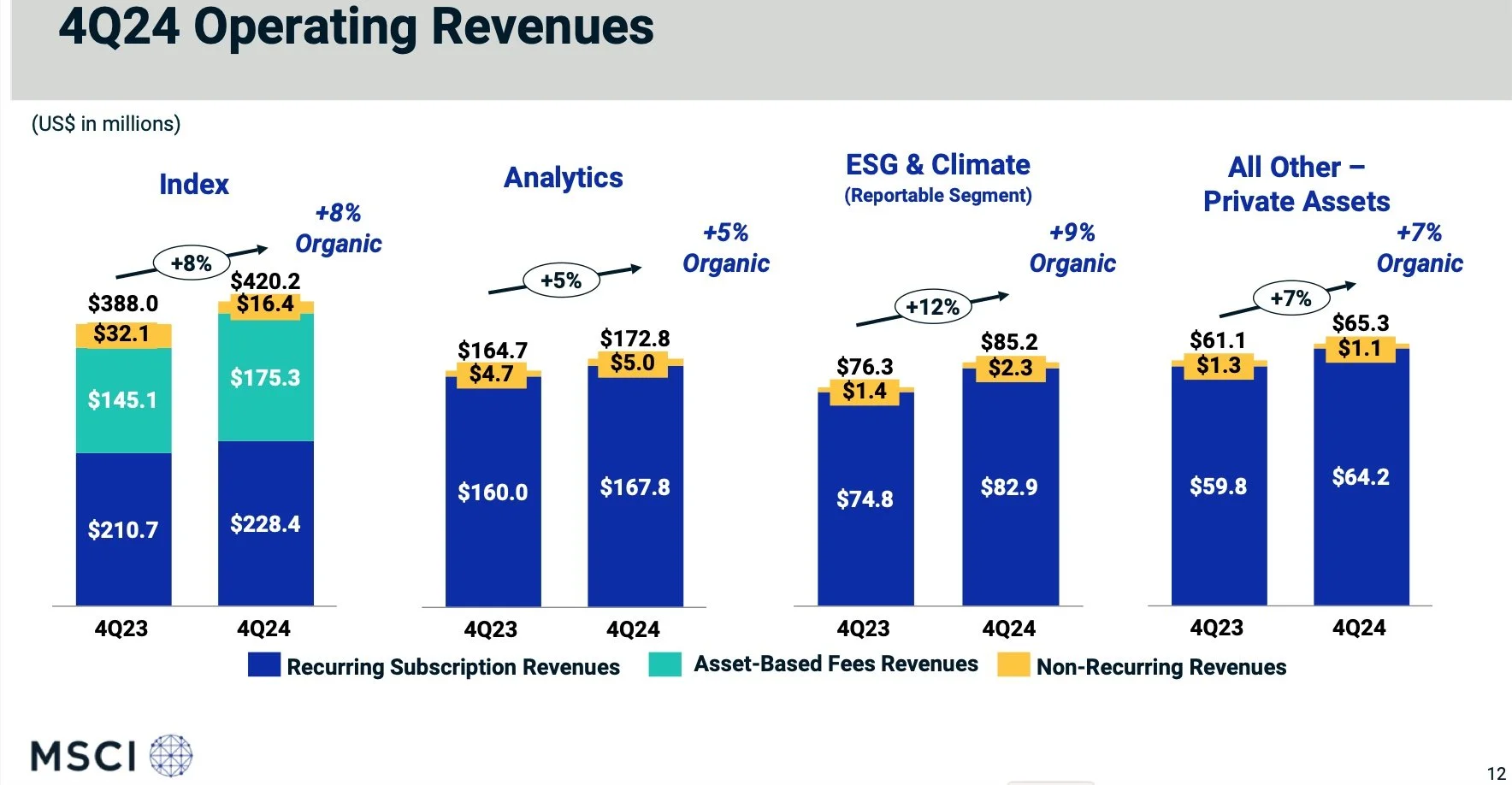

All ETF’s with the prefix “MSCI”, as in the MSCI All Country World Index (MSCI ACWI), earns a fee for MSCI Inc, either in the form of an annual recurring fee, or a fee based on the Assets under management in the ETF – on average 2.4 basis points of the AUM. The following slide from MSCI’s Q4 presentation details the organic growth in operating revenues, split by recurring and non-recurring.

Source: MSCI Q424 Investor presentation

The following is a brief overview of the basics of MSCI:

Reasons we find MSCI to be an attractive, quality company

The secular trend in the investment management industry to passive management strategies on the one hand, and more data driven active portfolios and strategies on the other. MSCI is well positioned to earn fees on both trends.

It operates as an oligopoly - as one of the 3 main providers of broad market indices.

Its high return in invested capital.

Recurring revenue comprises 97% of annual revenues at 31 December 2024.

Outstanding gross (82%) and operating (54%) margins.

Its growing number of indices, specifically those focussed on Private Capital, in all its different forms. MSCI has 266 indices tracking private assets, private equity, private real assets and private credit for different geographies, currencies and type. https://www.msci.com/documents/1296102/47386594/MSCI+Private+Capital+Closed-end+Fund+Indexes.pdf/79d9f60b-69c1-757a-67f6-c686f82c61cd?t=1719419727236

Converting more than its net income to free cash flow annually.

The low capital intensity – it requires very little additional capital to expand.

Management that has proven over time that they are sound allocators of capital and have delivered above market returns to their shareholders.

Areas for concern are not significant and mostly balance sheet related, with goodwill comprises 53% of total assets, reflecting historical acquisitions and a fair amount of serviceable debt. The current CEO has been managing the business for almost 30 years, we trust succession planning has been taken care of.

Valuation thoughts

At the current share price of USD 572.63, our valuation of MSCI Inc, at a discount rate of 10% and terminal growth rate of 3%, indicates an implied growth rate in Free Cash Flow of 14.05% over the next 10 years. Provided the dynamics for MSCI stays constant, our probability analysis is that MSCI Inc will grow its free cash flow between 10% to 12% annually over the next 5 to 10 years. At its current price, we estimate that MSCI is trading at a premium of 15% to 18% of its intrinsic value. There are better investments available at today’s prices.

Conclusion

We believe MSCI Inc to be a wonderful quality company. The industry in which they operate are encountering significant changes and they are well positioned to capitalise on the growth in passive index tracking investments as well at the significant growth in private assets. MSCI remains on our watch list.